Loan Approval Income Guidelines: How to Plan Your Loan Based on Annual Income

Welcome to our comprehensive guide on loan approval income benchmarks. In this article, you’ll learn how your annual income plays a crucial role in loan applications and how to plan a realistic repayment strategy that increases your chances of approval while protecting your financial health.

Why Annual Income Matters in Loan Planning

When applying for a loan—whether it’s for a mortgage, personal loan, or auto financing—lenders need to evaluate your repayment capacity.

Your annual income is one of the most important indicators they use to determine if you can handle the debt without falling into financial hardship.

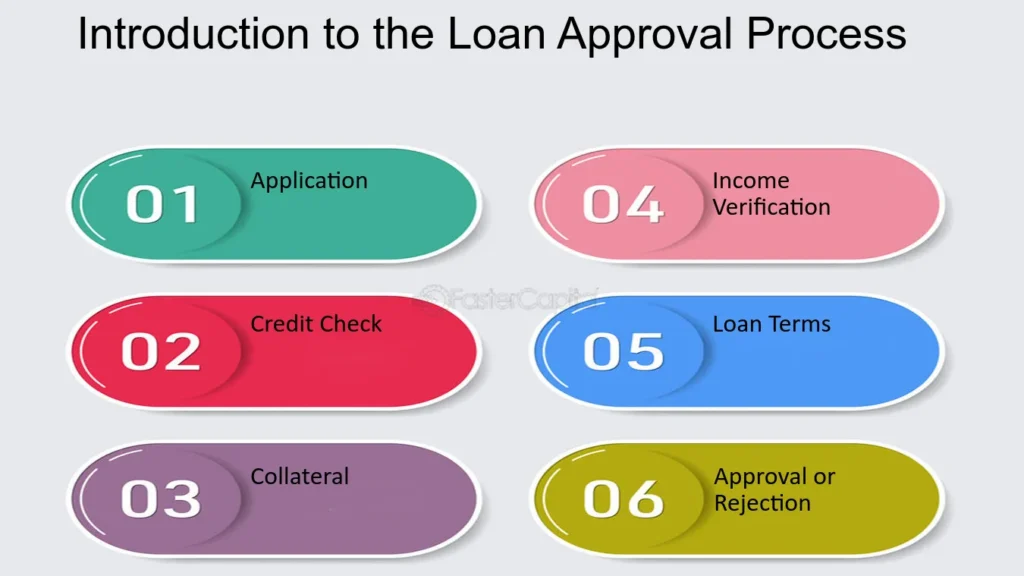

1. What Is the Loan Approval Income Guideline?

The loan approval income guideline is the benchmark financial institutions use to assess whether an applicant has sufficient repayment ability. This guideline considers factors such as your annual salary, employment stability, and existing debts to decide whether to approve your loan application.

2. Why Is Loan Planning Based on Annual Income So Important?

Aligning your loan amount and repayment period with your income ensures:

- You can meet monthly payments comfortably.

- You avoid excessive debt stress.

- You maintain financial flexibility for emergencies.

Proper planning helps you borrow with confidence—and repay without strain.

3. How Do Lenders Calculate Income Guidelines?

Financial institutions often use a debt-to-income ratio to determine eligibility. A common rule is that your annual loan repayments should not exceed 30% of your yearly income. However, criteria vary by lender, loan type, and interest rates.

Tip: Always compare offers from multiple banks or lenders before committing.

4. Benefits of Income-Based Loan Planning

- Accurate Repayment Ability Assessment: Provides a realistic picture of your capacity to repay.

- Reduced Financial Burden: Keeps monthly payments within manageable limits.

- Better Interest Rates: Higher incomes can sometimes qualify for lower interest rates or special offers.

5. Key Points to Keep in Mind

- Be Honest About Your Income: Providing false or exaggerated numbers can harm your approval chances.

- Self-Assess Before Applying: Make sure you can handle the loan even if your income changes.

- Plan for Flexibility: Choose a repayment schedule that leaves room for unexpected expenses.

Frequently Asked Questions About Loan Approval and Income Guidelines

Q: How much income do I need to get approved for a loan?

While exact requirements vary, a common benchmark is that your loan amount should not exceed three times your annual income. Always confirm with your specific lender.

Q: What are the most common repayment methods?

- Equal Principal Payments: The principal amount remains the same each month, with decreasing interest payments over time.

- Equal Total Payments: Both principal and interest are included in a fixed monthly payment.

- Lump-Sum Repayment: The entire amount is paid at once after a set period, usually with lower total interest costs.

Q: Should I choose a fixed or variable interest rate?

- Fixed Rate: Stability in monthly payments but sometimes slightly higher rates.

- Variable Rate: Can be cheaper if rates drop but riskier if they rise.

Choose based on your financial stability and risk tolerance.

Q: What is the ideal loan repayment period?

Typically between 10 and 30 years. Shorter terms mean higher monthly payments but less interest overall; longer terms lower your monthly cost but increase total interest paid.

Deja una respuesta